Implications of the Middle East conflict for the Spanish private sector

For too long, conflicts in the Middle East were perceived in Spanish boards of directors as distant tragedies, background noise that barely touched the bottom line. That era is over. The current escalation in the region is not an isolated event, but a systemic disruption that has blown apart the seams of globalisation as we knew it, forcing business leaders to redefine their risk management priorities. For Spain, a highly open economy dependent on energy imports, the relevance is immediate. We are not facing a simple statistical bump, but a signal of a fragmented international environment where geopolitics dictates economic results.

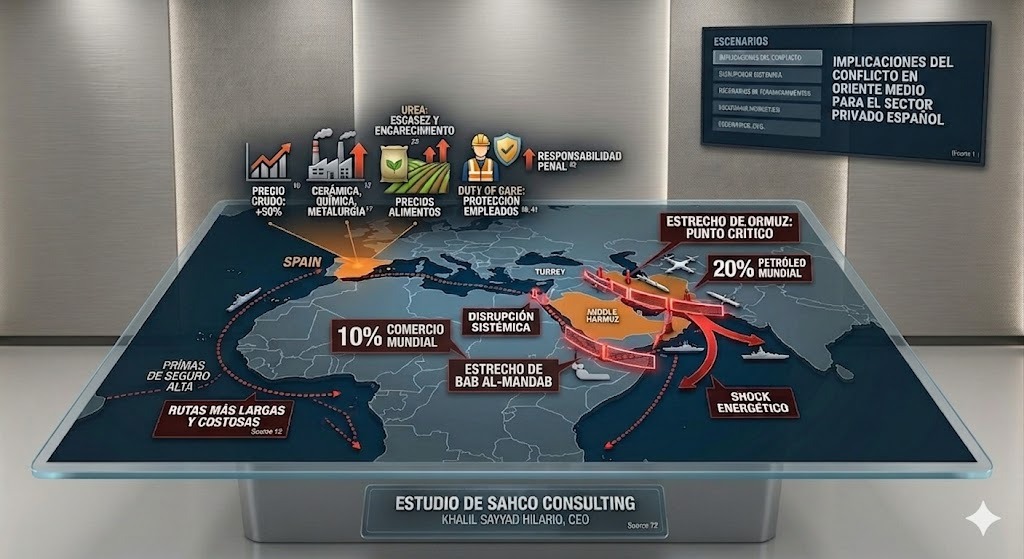

The energy jugular and logistical collapse

The heart of this crisis pumps through the strait of Hormuz, a critical point through which 20% of the world's oil and almost a fifth of liquefied natural gas passes. Drone and ballistic missile attacks, coupled with Iranian threats against maritime traffic, have transformed this corridor into a high-risk zone. The military response has been swift: from the deployment of warships to escort tankers to US aerial campaigns against targets such as Kharg island, responsible for 90% of Iran's crude exports.

This instability caused an immediate shock: the price of crude oil soared by 50% in the early stages. However, the damage is not just the price per barrel; it is the economic unviability of transit due to the increase in insurance premiums and the diversion towards longer and more costly routes. Strategic ports such as Jebel Ali have suffered interruptions, and the fragility of the Dubai hub , vital for trade and international aid, has jeopardised the just-in-time philosophy.

A board of vulnerable actors and sectors

The complexity of the conflict lies in its multipolar nature. The involvement of state and non-state actors, including Iran, Israel, the United States, Hezbollah, Iraqi militias, and the Houthis in Yemen, configures an arc of prolonged instability. This shockwave hits the Spanish industrial base hard. Energy-intensive sectors such as ceramics, chemicals, metallurgy, and transport see their margins evaporate under rising production costs. Even industries based on global mobility, such as international sport, entertainment, and the media, now face cancellations, venue changes, and reinforced security protocols to protect their teams in volatile areas.

From the field to the financial market

Perhaps the most insidious impact is the one not seen at first glance: fertilisers. The Gulf represents more than 30% of maritime urea exports. Its scarcity and rising cost directly hit the Spanish agri-food sector, especially cereals and export horticulture, pushing up food prices and compromising global food security.

At the macroeconomic level, these inflationary pressures reduce consumer purchasing power and weaken the import capacity of key markets for Spain. Added to this is the possible fall in remittances from the Gulf to Asia and Africa, and a financial environment where increased uncertainty raises risk premiums and the cost of capital, slowing down crucial investment decisions.

Scenarios and strategic perspectives

The evolution of the conflict is uncertain, but three main scenarios can be identified:

- First Scenario: A relatively quick de-escalation leaves behind persistent economic disruptions, with high energy prices in the short term and a gradual recovery.

- Second Scenario: The continuity of the conflict maintains tensions over energy production and maritime trade, prolonging inflationary pressures and weakening global growth.

- Third Scenario: A significant regional escalation, with a substantial reduction in energy exports and a negative impact on global economic growth, estimated at a fall of between 0.1% and 0.2% in 2026.

For Spanish companies, the message is clear: strategic resilience must take precedence over strict efficiency. This requires diversifying suppliers, reviewing logistical routes, and accelerating the transition to renewables. Paradoxically, amidst this volatility, opportunities arise for our companies in engineering, water management (critical for Gulf desalination plants), and energy infrastructure. In this new fragmented world, geopolitics is no longer an external risk; it is the board where the future of the business is played.

Implications for Security Risk Management, Duty of Care, and Crisis Management

The growing volatility of the geopolitical environment forces Spanish companies with an international presence to substantially reinforce their security risk management systems. This context poses critical challenges regarding the protection of employees, regulatory compliance, and the preservation of corporate reputation.

- Duty of Care: The duty of care (diligence) towards employees acquires strategic centrality. In the Spanish legal system, this derives from the Law 31/1995 on the Prevention of Occupational Risks, which establishes that the employer must guarantee the safety and health of workers in all aspects related to work. This obligation is not limited to national territory but extends to international travel and expatriations.

- Legal Responsibility: The framework of criminal liability for legal entities (Article 31 bis of the Spanish Penal Code) establishes that companies can be held criminally liable if they have not implemented adequate management models. The absence of protocols for protection or evacuation can lead to criminal or civil liabilities.

- Reputational Risks: A serious incident affecting employees, such as kidnappings, injuries, or deaths, can have a significant impact on public perception and investor confidence.

Therefore, security risk management must be structured around three fundamental axes: prevention, response capacity, and crisis management. This includes specific risk assessments by country, real-time monitoring systems, and formal crisis management structures with defined roles.

Final strategic reflection

The conflict in the Middle East redefines strategic priorities in terms of corporate security and the protection of people. For the Spanish private sector, this implies assuming that the protection of employees forms part of the core of corporate responsibility. In many cases, this transformation requires going beyond the internal capabilities of organisations, making it advisable to turn to external actors with specific expertise in corporate security, risk intelligence, and crisis management. Ultimately, business resilience will increasingly depend on the ability to integrate economic, operational, and security risks into a coherent strategic vision.

Khalil Sayyad Hilario

Founder & CEO SAHCO Consulting

Madrid, 2nd April 2026

Contacter SAHCO

Pour en savoir davantage sur notre expertise et le déroulement de nos missions.